Two numbers tell you most of what you need to know about reshoring right now.

The first is 58%.

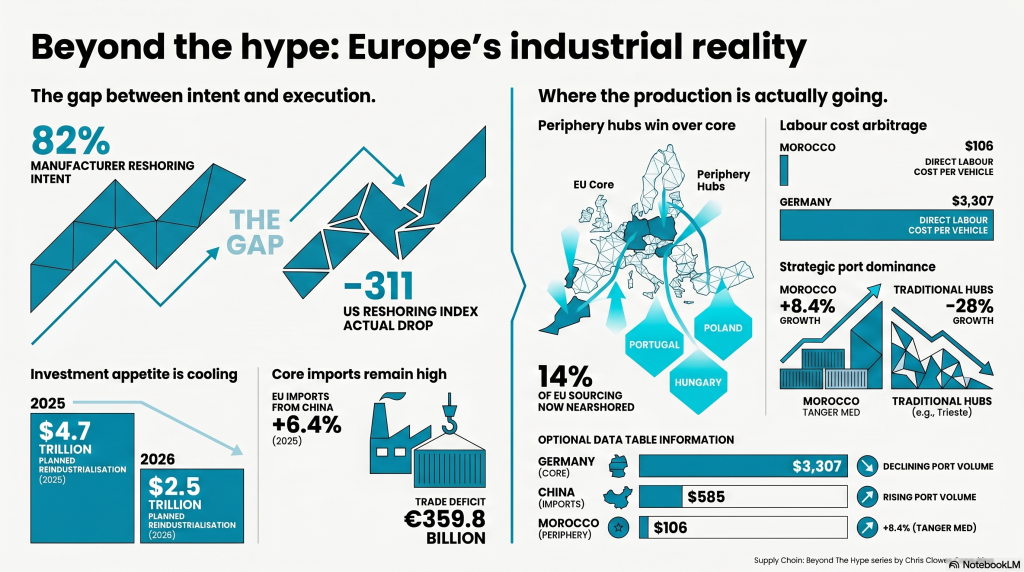

That is the share of UK manufacturers who told Medius they are actively reshoring, with 82% planning to accelerate. Add Make UK’s survey, where 70% of British manufacturers expect reshoring to pick up further under the new industrial strategy, and Capgemini’s latest research showing European and US executives still committing trillions to reindustrialisation, and you have the most confident boardroom consensus on industrial policy in forty years.

The second is minus 311.

That is the points drop in Kearney’s 2025 US Reshoring Index, which tracks actual import flows rather than surveyed intent. Imports from 14 Asian low-cost countries grew 10% in 2025, while US domestic manufacturing output crept up 1%. ING’s November 2025 eurozone analysis is blunter still, noting “very limited evidence of actual reshoring activity” across the single currency area. EU imports from China rose 6.4% in 2025 to €559.4 billion, widening the bilateral deficit to €359.8 billion. And Capgemini’s own 2026 edition, published this month, shows planned investment over the next three years has fallen from $4.7 trillion in 2025 to roughly $2.5 trillion in 2026. The appetite for strategy is up, the appetite for actually spending the money is way down.

Both sets of numbers are correct, because surveys measure what boards intend to do, and import and investment data measure what procurement teams and CFOs actually sign off. The gap between intent and execution has become the single most important piece of context for any supply chain leader planning a 2026 sourcing strategy.

There is a third number that matters more than either of them, however, and that’s 14%.

That is the share of EU sourcing that QIMA recorded as nearshoring or reshoring in 2025, an all-time high, with Mediterranean inspection demand up 25% year on year. Production is genuinely moving, but it is moving somewhere very specific. Not Birmingham, Stuttgart or Lyon. It is moving to Tangier, Debrecen and Porto. Europe’s industrial revival, to the extent there is one, is happening on the continent’s periphery rather than in its historical core.

Where the production is actually going

The verifiable data, the stuff you can count in shipping manifests and factory openings, tells a consistent story. The winners are Morocco, Egypt, Poland, Hungary and Portugal. QIMA’s 2025 inspections, drawn from more than 30,000 clients, show Egypt inspection demand up 52% year on year, Morocco up 38% and Tunisia up 18%. Turkey is a notable absence. QIMA’s own analysts flagged that Turkish textiles struggled with rising costs and labour shortages in 2025, and orders that might historically have gone there were reallocated to Egypt and Morocco. These are not opinions from survey respondents, they are confirmed purchase orders on their way to being shipped.

Port data confirms the same pattern. Morocco’s Tanger Med handled 11.1 million TEUs in 2025, up 8.4%, with net profit jumping 22.3%. Slovenia’s Luka Koper set a record at 1.27 million TEUs, up 12%, on the back of hinterland supply into Central European factories. Piraeus, the traditional Asia-to-Europe gateway, saw container volumes fall 6%, and Trieste Marine Terminal had its worst year since 2016, dropping more than 28%. The traffic is leaving the eastern Mediterranean and concentrating in the western Med and the Adriatic, precisely where the new production is being installed.

The anchor investment is Stellantis at Kenitra. A €1.2 billion expansion inaugurated last July doubled capacity to 535,000 vehicles and allocated €702 million specifically to local supplier development. Morocco’s automotive exports hit a record $17 billion in 2024, already the largest industry on the African continent. The labour economics explain the rest. Oliver Wyman’s 2025 benchmark found Morocco produces a vehicle for $106 of direct labour cost, against $585 for Chinese manufacturers and $3,307 in Germany. Tanger Med has been running on 100% green electricity since January 2025 and has deep-water capacity for the ultra-large container vessels diverted round the Cape of Good Hope. The geography, the wage structure and the infrastructure stacked up just as the Red Sea fell over. That is not a coincidence, it is causation.

Why the heartland isn’t getting its factories back

The contrast with Europe’s industrial core is sharp, and the battery sector illustrates it painfully. Northvolt, the EU’s flagship home-grown gigafactory, filed for bankruptcy in March 2025 despite billions in project financing, including roughly €940 million of European Investment Bank backing. The Skellefteå plant has been sold to Lyten, an American lithium-sulfur battery firm. Meanwhile the dominant new battery builds in Europe are Chinese-financed. CATL’s €7.3 billion, 100 GWh plant in Debrecen, Hungary, is set to start production this year with 9,000 workers. The CATL-Stellantis joint venture in Zaragoza, 50 GWh of LFP capacity, starts late 2026.

A CATL plant in Hungary counts as European production on the press release, but it is Chinese capital, Chinese intellectual property and, in many cases, Chinese technical leadership operating on European soil with EU state aid behind it. McKinsey estimates Europe produces less than 10% of global battery cell capacity, and is misaligned on chemistry too, focused on NMC while demand is pivoting to LFP. The industrial base that was supposed to underpin Europe’s reshoring ambition has, in practice, become a licensing arrangement with the supplier everyone was trying to de-risk from.

The tailwind is fading

Two shifts are easing the pressure that drove the 2024 and 2025 moves, just as the contracts signed on that basis hit execution.

The Gemini Cooperation, Maersk and Hapag-Lloyd’s new alliance launched in February 2025, is delivering schedule reliability averaging around 90% in its first year, well ahead of an industry norm closer to 60%. That removes one of the biggest operational arguments for nearshoring, which was that long-haul Asian supply chains had become fundamentally unpredictable. And Suez is tentatively reopening. The October 2025 Gaza ceasefire brought major carriers back for the first time in two years, and canal revenue in the first quarter of the 2025/26 Egyptian fiscal year was up 18.5% year on year. Traffic is still roughly 60% below normal, but the direction of travel is clear.

Which puts the nearshoring moves of the last eighteen months to an immediate test. A Stellantis gigafactory at Kenitra is not reversible. A procurement memo about dual-sourcing very much is. We are about to find out which commitments were strategic and which were tactical.

What separates the moves that stick

Three operational patterns distinguish the nearshoring that is holding from the nearshoring that is wavering. Labour cost under €15 an hour, a pre-existing supplier ecosystem, and deep-water port access. Morocco stacks all three. Hungary has the labour and suppliers but relies on Chinese capital for the headline projects. Turkey has proximity and scale in textiles but has lost ground to Egypt on cost. The UK, for all the surveyed enthusiasm, has very little of any of these, and labour costs several multiples above those in Bulgaria, Romania or Morocco. The firms getting this right committed capital before they announced strategy. The firms still struggling announced strategy before they committed capital.

5 Key takeaways for supply chain leaders

- Treat survey data with care. Intent metrics are running 20 to 30 percentage points ahead of physical reality. If your board assumes competitors are moving at the pace the surveys suggest, you are overestimating the shift.

- The real action is on the periphery, not the core. If you are planning a nearshoring move this year, your best options are Morocco, Portugal, Poland or Hungary, not a domestic repatriation. The wage differential combined with EU trade access is decisive.

- Supplier qualification is the binding constraint. Stellantis put €702 million into Moroccan suppliers alongside the plant expansion. The firms that have moved most successfully invested in local supplier development years before announcing the move. Without that, a new factory is just a shell.

- Geography still wins. Tanger Med, Koper and Gdansk are absorbing volume because they combine labour arbitrage, EU trade access and port infrastructure in the same place. Inland sites without port access are losing out, even where the labour economics work.

- Stress-test your business case against Suez reopening. Freight reliability is returning and long-haul shipping is looking more predictable than it has since 2023. Plan for a scenario where Asian sourcing looks economically attractive again by mid-2026, and make sure your nearshoring case stands up against that.

Final thoughts from me

What I keep coming back to with clients is the discipline of separating what is genuinely rewiring from what is posturing. In most of the companies I work with, reshoring has become a category on a strategy slide rather than a line item in a capital plan. That is fine as a hedge, but it does not change the supply chain. What changes the supply chain is a signed contract, a qualified supplier and a production line with an installation date.

If we look back on this period in five years, I suspect we will see 2024 and 2025 not as the start of European reindustrialisation, but as the period when Europe’s periphery cemented its place as the continent’s new industrial spine.

The question worth putting to your own team is whether your next sourcing decision reflects where the factories actually are, or where you wish they were.